Deglobalization and Investing: How Structural Shifts Are Redefining Markets and Why Active Management Matters Now

Written by: Kasey Wopperer, Co-Founder and CIO of Stone Creek Advisors

Written on February 26, 2026

Key Takeaways

Globalization peaked in 2008 and has stagnated since.

Trade fragmentation is reshaping inflation, supply chains, and capital flows.

Passive strategies were optimized for global integration.

Rising geopolitical divergence increases dispersion and volatility.

Active management becomes critical during structural regime shifts.

Throughout my career, I have been drawn to the study of long-term structural forces. In 2011, I was tasked with building a bullish case for the U.S. economy. That assignment became a turning point. As I dug deeper, I found compelling evidence of a potential U.S. manufacturing renaissance, supported by rising automation, and the early signs of an American energy resurgence. At the same time, the Japanese tsunami exposed the fragility of hyper-efficient global supply chains. The pandemic and the war in Ukraine later revealed the national security risks and supply disruptions that come with relying too heavily on distant partners for critical goods and resources.

I came to believe we had reached peak globalization. That research became the intellectual foundation of Stone Creek Advisors and has shaped our portfolio construction. For decades, globalization, demographic dividends, falling corporate tax rates, and declining interest rates created powerful tailwinds for growth and asset prices. In that regime, disciplined stock selection could thrive without much concern for the broader macroeconomic backdrop. But at inflection points, the macro matters. When structural tailwinds slow or reverse, they can overwhelm even the strongest fundamentals. What once supported valuations can begin to compress them.

Recent developments in U.S. trade policy, including Liberation Day and its aftermath, have accelerated a transition that had already begun. The tailwinds that defined the last era are no longer reliable. We believe we are at a structural turning point that could shape markets and portfolios for years to come.

For nearly four decades, globalization was the defining force of modern economics. Cross-border trade expanded, supply chains became increasingly complex and interconnected, capital flowed with unprecedented ease across borders, and consumer bases and labor markets globally became accessible to companies. Ever-deepening global integration delivered consistent returns in this environment of declining friction and expanding markets. That era is ending.

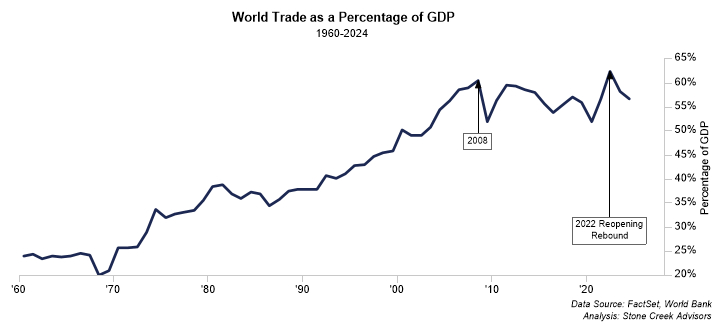

Has Globalization Peaked?

The World Bank chart below shows global trade as a percentage of GDP peaked in 2008 and has since stagnated, aside from a temporary reopening rebound in 2022. Geopolitical fragmentation has accelerated with trade restrictions and economic sanctions becoming more routine policy tools. Supply chain localization, once dismissed as inefficient, is now a strategic priority for both corporations and businesses. Foreign direct investment flows have declined as a share of global GDP from 5.3% in 2007 to 1.3% in 2024, according to The World Bank [1].

The old playbook, where globalization acted as a secular tailwind for growth and a structural headwind to inflation, is being rewritten. This is not a cyclical disruption, but a structural change in how markets, policy, and capital interact. SCA believes globalization has peaked, a transition that could reverberate through economies, asset prices, geopolitics, and risk premia.

Tariff Shock and Policy Driven Uncertainty Alter the Landscape

In Everybody Freeze, we warned unprecedented tariff levels would stall corporate decision and delay investment. That uncertainty proved persistent. After tariff renegotiations, effective tariff rates remained elevated, acting as a tax on global commerce.

Policy-driven uncertainty slowed economic momentum and softened labor markets, even as headline indices appeared resilient. Yet markets, conditioned by past cycles, often chose to look through these signals, supported by expectations of policy accommodation.

From Optimization to Resilience

The era of cost centric, globally optimized supply chains is giving way to resilience-focused structures. Companies are diversifying suppliers, increasing inventories, reshoring strategic production, and prioritizing security of access over lowest cost production. Hyper-efficient global sourcing, once a competitive advantage, is now viewed as a potential vulnerability.

This shift has been building for over a decade. As China moved up the value chain, intellectual property concerns intensified. Automation reduced the relative importance of labor cost arbitrage. Transportation costs and delivery timelines became a bigger portion of the cost equation, a cost that is much less predictable. Long supply chains increased time to market and threatened first-mover advantages. These pressures gradually pushed companies to consider moving production closer to home.

Inflation and Monetary Implications

Globalization exerted sustained downward pressure on goods prices by allowing companies to tap global labor and production capacity. Deglobalization alters that dynamic. Without the ability to relieve domestic constraints through global sourcing, inflationary cycles may become more frequent.

Deglobalization refers to the slowing or reversal

of cross-border trade, capital flows, and supply chain integration,

leading to regionalization and geopolitical economic blocks.

This is not inflation driven purely by excess demand. It is inflation that reflects the higher cost of operating in a fragmented global system. In this environment, the Federal Reserve may be forced to intervene more frequently to contain inflation, potentially resulting in shorter economic cycles and greater volatility.

Deglobalization Means Fragmentation, Not Isolation

The global economy is not collapsing, it is fragmenting. Trade flows will continue, but increasingly along geopolitical lines. Supply chains are regionalizing and capital will become more selective. Economic blocs are forming based on strategic alignment rather than pure efficiency.

For investors, this means analyzing multiple centers of gravity instead of assuming a single synchronized global expansion. There will be winners and losers from a country perspective in this new world.

Portfolio Implications

The investment consequences of this transition are significant.

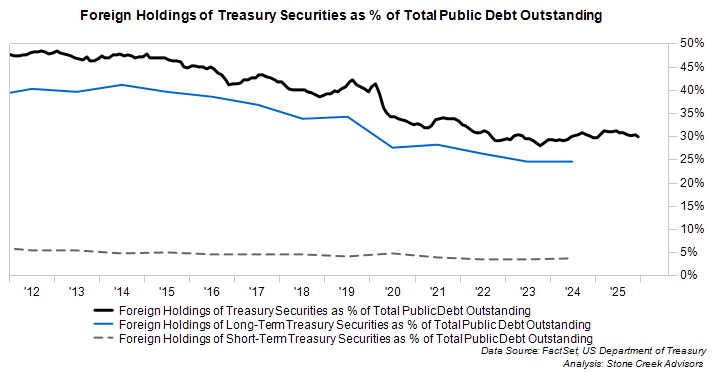

Using data from the US Department of Treasury, roughly 30% of U.S. Treasuries are held by foreign investors, many in longer-dated maturities. This is down from over 45% over a decade ago. If global central banks continue to reduce their demand or reallocate reserves, upward pressure on yields could follow. In recent years, central banks around the world have steadily increased gold purchases as they diversify reserves, a trend we expect to continue.

The United States has long commanded valuation premiums to other markets. As global dynamics shift, so too could the strength of the dollar and the multiple investors are willing to pay for U.S. assets. Multinational corporations that rely heavily on global consumer bases may face revenue headwinds in a more fragmented world.

Passive, buy-and-hold strategies were optimized for an era of expanding integration and declining friction. Several assumptions underlying those strategies become less reliable in a deglobalizing environment:

Market correlations may weaken as economic blocs diverge

Volatility may increase as geopolitical events carry systemic consequences. Nations are more likely to go to war with each other as they become less economically dependent on one another.

Sector leadership may rotate as globalization winners face structural headwinds

If dispersion increases and correlations become unstable, broad index exposure becomes a less precise solution.

Why Active Management Matters

In this environment, active management that takes the economy into account becomes a necessary component of a comprehensive wealth strategy. The skills required to navigate contracting globalization are precisely those that strategic active management provides:

Dynamic allocation: Active managers can adjust portfolio composition as geopolitical and economic conditions evolve. This flexibility allows for positioning ahead of policy shifts rather than reacting after markets have adjusted.

Bespoke risk assessment: Evaluating geopolitical risk, regulatory trajectory, and supply chain resilience requires qualitative judgment that cannot be captured by an index. Active managers can incorporate these factors into security selection and portfolio construction.

Opportunistic positioning: Market dislocations created by deglobalization may generate mispricing that active strategies can exploit. As market structure fragments, the dispersion of returns within asset classes increases, creating opportunities.

Concentration management: Passive strategies can result in unintended concentration risks. Today, the S&P 500 is more concentrated than at any point in history [2]. Passive strategies can create unintended exposure to concentrated risks at precisely the moment structural forces are shifting. Active management allows for deliberate risk budgeting that accounts for changing correlations and tail risks, which is critical for wealth preservation.

Portfolios must be built to endure uncertainty, not merely to outperform in ideal conditions.

The Path Forward

Deglobalization represents a structural shift that extends far beyond trade statistics, altering inflation dynamics, capital flows, fiscal priorities, market leadership, and geopolitical relationships.

The assumption that markets naturally tend toward efficiency and that historical patterns provide reliable guidance is less certain when the underlying economic structure is changing. Regime changes unfold gradually. Markets adapt unevenly. Narratives lag reality. Yet once the underlying shift becomes visible, capital allocation patterns can change for years.

Strategic active management provides the tools necessary to navigate this transition: dynamic allocation, qualitative risk assessment, and the ability to exploit market dislocations. These capabilities are not luxuries, but requirements for preserving and growing your legacy.

The organizing principle of the past several decades was economic integration. The emerging principle is strategic alignment and resilience.

At SCA, our investment approach is designed to navigate this transition with deliberate active management, geopolitical awareness, and dynamic risk management across asset classes.

If you are reassessing your portfolio strategy in light of these structural changes, we welcome the conversation. The investment landscape has shifted. Your legacy deserves a strategy built for the world as it is becoming, not the world that once was.

[1] Foreign direct investment, net inflows (% of GDP) | Data Source: the World Bank

[2] Source: 2025 Year-End Review CIO Letter & 2026 Investment Outlook: Positioning to Endure—Not Just Perform. S&P 500 Index Concentration chart: Weight of the top 10 companies in the S&P 500. Source: JP Morgan Asset Management

Stone Creek Advisors is a DBA of OneSeven, an investment adviser in Ohio. OneSeven is registered with the Securities and Exchange Commission ("SEC"). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. OneSeven only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of OneSeven's current written disclosure brochure filed with the SEC, which discusses OneSeven's business practices, services, and fees, is available through the SEC's website at: www.adviserinfo.sec.gov. All titles listed for Individuals associated with Stone Creek Advisors represent the individual's role with Stone Creek Advisors.

Please note, the information provided in this presentation is for informational purposes only and investors should determine for themselves whether a particular service or product is suitable for their investment needs. Please refer to the disclosure and offering documents for further information concerning specific products or services. Investments in securities entail risk and are not suitable for all investors. Past performance is not a guarantee of future returns. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.