2025 Year-End Review CIO Letter & 2026 Investment Outlook: Positioning to Endure—Not Just Perform

Written January 9, 2026

As we close out 2025, it is worth stepping back and reflecting on just how unusual this year has been. Markets spent much of the year behaving as though certainty was abundant, even as the underlying economic, political, and financial signals suggested otherwise. Equity indices finished near highs, volatility remained suppressed for long stretches, and investor sentiment oscillated between optimism and complacency with only brief bouts of bearishness. 2025 closed out a third consecutive year of double-digit returns in the S&P 500. Yet beneath the surface, the forces shaping the next part of the cycle continued to build.

2025 in Review: Calm on the Surface, Stress Below

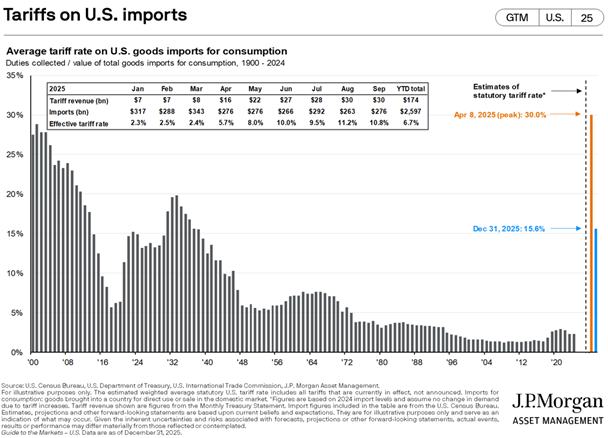

The defining feature of 2025 was not growth or inflation, but policy-driven uncertainty. The tariff regime introduced early in the year shocked the system, freezing corporate decision-making and forcing companies and consumers to wait for clarity that never truly arrived. The JPMorgan chart below depicts the effective tariff rate. Tariffs really began hitting in the second half of Q2 and continued to trend higher with the implied December 31st tariff rate suggesting that path is set to persist in Q4. Negotiations continue, but the outcome could keep the effective tariff rate above the 10ish% of Q3.

As the year progressed, markets learned to live with the uncertainty and ascended a wall of worry already built on a peak. Investors grew increasingly comfortable assuming any sign of weakness would be met with policy support. This belief helped propel risk assets higher, even as:

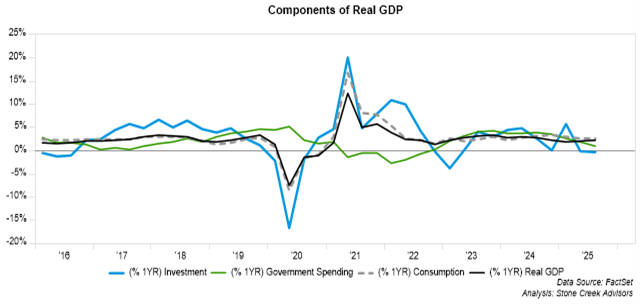

Economic growth slowed, with real GDP hovering near 2% and increasingly reliant on consumption funded by transfer payments, declining savings, and rising debt.

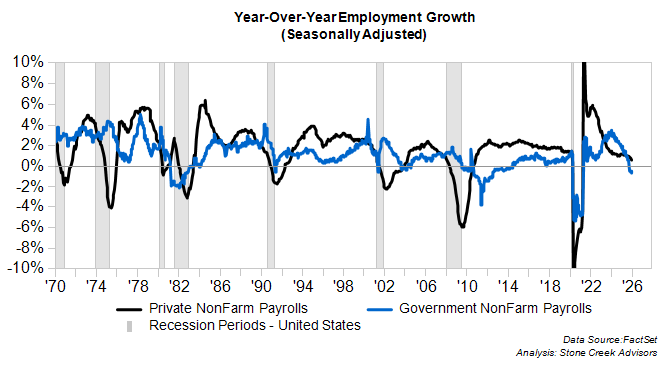

Labor market strength softened, masked by public-sector hiring and declining participation rather than true private-sector momentum. We expect this will be even more pronounced after the revision to payrolls in February.

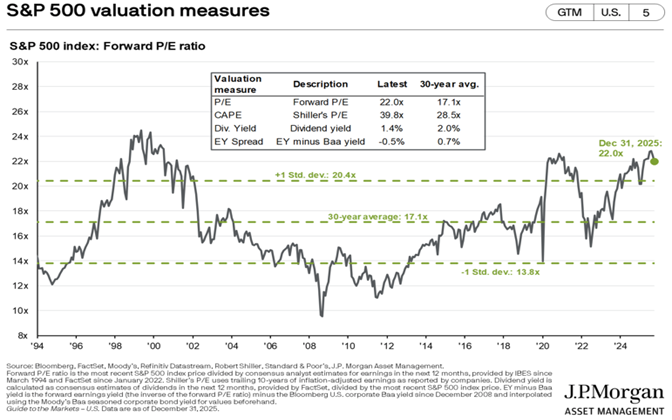

Valuations expanded, pushing U.S. equities further into historically expensive territory with little margin for disappointment.

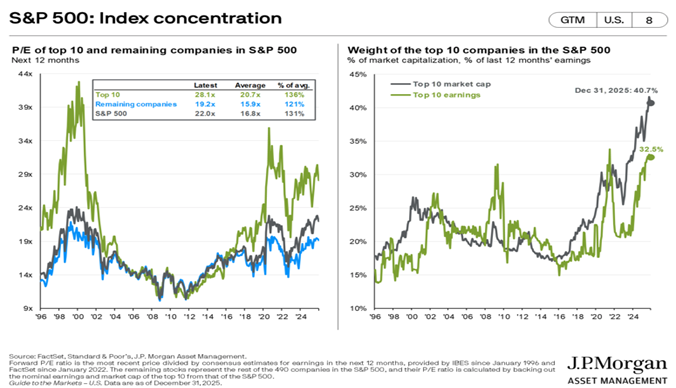

Market concentration reached extremes, leaving broad indices vulnerable to narrow leadership and crowded positioning. When an investor buys the S&P 500 today, they are putting 41% of their new money in the top 10 holdings, a slice of the market that is trading at a P/E of 28.1x.

At the same time, warning signs accumulated under the surface. High-yield credit spreads began to widen, delinquency rates rose across consumer categories, liquidity conditions tightened, and long-term Treasury yields climbed not because of growth optimism, but perhaps because of inflation concerns and investors demanding greater compensation to fund persistent and growing deficits.

Since the Federal Reserve began cutting interest rates in September 2024, the 10-year Treasury yield has risen slightly, and the 30-year Treasury yield has risen significantly. This is the opposite of what President Trump wants as the 10-year yield directly impacts economic activity.

Gold’s surge throughout the year, its strongest performance since the late 1970s, was not a coincidence. It reflected a growing recognition that the monetary and fiscal backdrop is changing, and that traditional anchors of stability can no longer be taken for granted.

The Fed, Fiscal Reality, and Fragile Confidence

The Fed entered 2025 constrained, and it exited the year no less so. Rate cuts resumed, but not from a position of strength. The Fed finds itself balancing deteriorating labor market conditions against inflation that remains structurally higher than in prior cycles, all while operating under the shadow of political pressure and rising questions about fiscal sustainability and independence.

Meanwhile, government deficits continued to expand, Treasury issuance remained heavy, and foreign demand for Treasuries in countries like China continued to sour. Historically these dynamics have mattered. Markets that thrived on abundant liquidity and unquestioned confidence are increasingly sensitive to credibility, discipline, and balance-sheet health.

Investment Through 2025

High and increasing asset prices do not eliminate risk, but they often disguise it. It is impossible to time the exact moment when these things will start to matter. This is why staying invested is important. However, staying invested does not have to mean having a static portfolio. It is still possible to avoid the most expensive and riskiest areas of the market while participating, which has been our goal over the past two years. This allows our clients to participate in most of the market appreciation, while giving them some protection if the market wakes up. We focus on risk-adjusted returns and in this type of momentum driven market we are prioritizing downside protection.

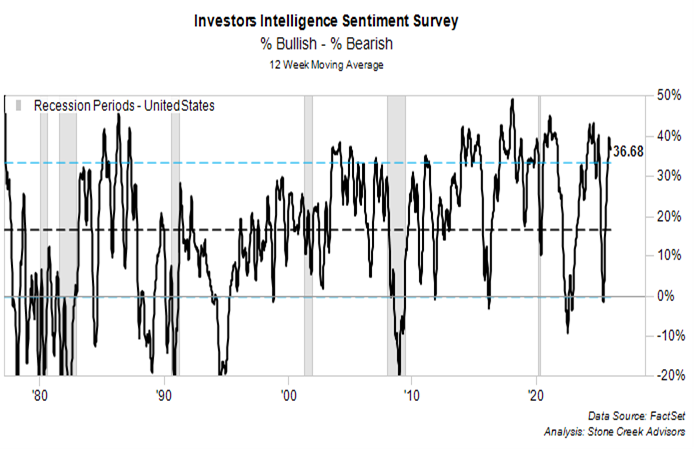

Periods of complacency can persist longer than expected, but they rarely end smoothly and the change in sentiment often comes quickly. The chart below suggests investor sentiment is very complacent today. A high percentage of investors responded as currently bullish on the market and only a low percentage are currently bearish, leaving the spread over a standard deviation above the mean.

The disconnect between asset prices and fundamentals widened last year, reinforcing our belief that risk management matters most when it feels least urgent. Throughout 2025, our approach remained consistent:

Emphasizing diversification across asset classes and geographies.

Favoring quality, balance-sheet strength, and durable cash flows.

Maintaining liquidity and downside protection.

Avoid areas where optimism has outrun reality.

Taking advantage of opportunities where we believe the markets have overreacted to negative news.

While we remained underweight equities versus our benchmarks, our sizeable position in gold helped us participate well in 2025’s market rally. The headline market was strong but there were numerous areas of the market that did not participate. This gave us opportunities to add some very good companies at compelling prices to our portfolio throughout the year.

2026 Market Outlook: A Narrow Path

As we look to 2026, we see a narrowing path forward. The range of possible outcomes remains wide, but the margin for error is thin. Sell-side analysts are decidedly bullish, expecting 15% earnings growth in 2026 for the S&P 500. With valuations near historic highs, 2026 market returns are more likely to have to come from earnings rather than multiple expansion.

The impacts of the One Big Beautiful Bill Act should be net positive for equities in 2026, Germany is actually spending money, the Fed is loosening monetary policy and providing some liquidity, and the Artificial Intelligence boom is still on. While the risks surrounding the AI boom are well known, none are currently being factored into valuations or expectations. Artificial Intelligence will likely continue to be the theme of 2026. Will this “revolutionary” technology increase productivity, margins, and earnings growth enough to overwhelm the labor market implications of this new efficiency? Will investment spending from companies continue to expand at the pace it is expected to and will that fuel economic growth?

The market is answering with an enthusiastic “Yes”. Even with all the risks, it is difficult to be too negative on equities due to the possibility that everything does turn out right. The capital expenditures are massive; these tech firms are finally deploying cash that they have been hoarding on their balance sheets. “Hyperscalers” collectively invested over $100 billion in Q3 capex according to data pulled by Y Charts. If investors maintain a patient stance, and do not increase their scrutiny of AI spending, this party may continue. This has kept us cautiously exposed to, yet underweight, the AI trade. We recognize the risk of being overexposed but also recognize the risk of having no exposure, therefore we have an allocation which we adjust as valuations change. However, we are avoiding the very speculative areas.

This is where our ability to be both top-down and bottom-up has given us a distinct advantage. Our Director of Investments, Peter, filters through the universe and picks the areas we want exposure to and avoids the areas that are too risky. Our ability to be nimble and trade at a moment’s notice has also been helpful in this environment and we expect that to continue to be the case.

Under the surface, there are many factors that could derail the ride, and valuations have left little room for error. Swerving today without a shoulder or guardrails could be disastrous. Several themes may shape the year ahead:

Growth Will Likely Remain Fragile: The economy enters 2026 without a strong buffer. Consumption is stretched, business investment remains cautious, and fiscal support faces growing constraints. A modest slowdown could have outsized effects. We remain overweight the more defensive sectors of the market for this reason.

Inflation May Prove Stickier Than Expected: Tariffs, supply chain realignment, geopolitical risk, and energy constraints all point toward structurally higher and more volatile inflation. This limits the Fed’s ability to respond aggressively to downturns. We continue to have exposure to areas of the market that can do well in inflationary and stagflationary environments for this reason.

Valuations Matter Again: With U.S. equities priced for near-perfect outcomes, future returns will depend far more on earnings delivery than multiple expansion. Disappointment risk is asymmetric. We are avoiding the most overvalued parts of the market and focusing on areas where the growth outlook is underappreciated or outright negative.

Earnings are Going to Need to Match Expectations: Multiples are unlikely to continue to increase much from current levels. Therefore, returns are going to have to come from earnings growth following through. We are avoiding the areas of the market where we feel expectations are unattainable.

Global Opportunities Are Increasingly Attractive: Relative valuations and cyclical positioning abroad, particularly in developed international markets, offer better risk-adjusted opportunities than the most crowded areas of the U.S. market. We began shifting exposure internationally at the end of 2024 and expect this will continue.

Liquidity Will Be a Key Driver: Markets are increasingly sensitive to shifts in liquidity. Episodes of stress may emerge quickly and without warning, creating both risk and opportunity for disciplined investors. We still have a healthy buffer of dry powder to deploy as opportunities emerge and we are avoiding the more illiquid areas of the market.

Geopolitical Tensions Will Stay in the Headlines: Venezuela is the new headline. However, we are seeing large military drills by China that leave a concern that China may be closer to invading Taiwan. We are also seeing many large nations ramp up military spending, most recently Japan. This will continue to support gold prices and our exposure to large defense contractors.

Positioning for an Uncertain Year

In this environment, we believe success in 2026 will depend less on predicting a single outcome and more on being prepared for a range of outcomes.

Our focus remains on:

Defensive equities with pricing power and resilient earnings

Dividend growth as a source of real return

Short-term Treasuries and gold as ballasts of the portfolio

Select international exposure where fundamentals and valuations align

Patience—waiting for opportunities created by volatility rather than chasing momentum

Driving faster does not improve visibility in the fog, it increases the cost of an error. As we enter 2026, prudence, discipline, and flexibility matter more than speed.

The surface may still look calm, but the currents underneath remain strong. Whether markets continue forward smoothly or encounter sharper bends ahead, our responsibility is the same: to steward capital thoughtfully, protect against permanent loss, and position portfolios, not just to perform, but to endure.

As always, thank you for your trust and partnership. Please reach out with any questions.

Kasey

One Seven (“One Seven”) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training. Services are provided under the name Stone Creek Advisors, LLC, a DBA of One Seven. Investment products are not FDIC insured, offer no bank guarantee, and may lose value.