2026 Second Quarter CIO Letter: If Scarcity Ends

The first half of 2026 has rewarded optimism. Earnings strengthened, AI investment continues to accelerate, and markets have recovered to new highs.

Momentum and leverage have reached historically elevated levels. Expectations leave less room for disappointment than they have in several years.

Today's market may be entering a new phase. For nearly twenty years investors benefited from shrinking public equity supply. That tailwind may now be reversing.

Future returns may depend less on multiple expansion and more on free cash flow generation, capital allocation, and returns on invested capital.

Technology revolutions create enormous wealth, but they have historically also attracted too much capital. AI may ultimately follow a similar path.

We remain constructive on long-term innovation while emphasizing diversification, valuation discipline, and businesses capable of generating durable free cash flow.

2026 First Quarter CIO Letter: A Narrowing Path

In the first quarter of 2026, markets continue to navigate a more complex and constrained environment, where opportunities are increasingly selective and risks less forgiving. In this CIO letter, we examine the forces shaping today’s landscape—from narrowing market leadership to evolving macroeconomic pressures—and what they mean for portfolio construction. As the path forward becomes less broad and more defined, disciplined positioning and thoughtful risk management remain essential.

Borrowing Against Your Investment Portfolio: Benefits, Risks, and Lombard Lending Strategies

Borrowing against your portfolio can create liquidity without selling assets—but it introduces risks that must be carefully managed. From margin calls to leverage exposure, this strategy requires discipline and a clear understanding of when it truly makes sense.

This article explores how securities-based lending works, where it can go wrong, and how to approach it thoughtfully within a broader wealth strategy.

Deglobalization and Investing: How Structural Shifts Are Redefining Markets and Why Active Management Matters Now

For decades, globalization acted as a powerful tailwind for markets, driving efficiency, expanding trade, and supporting steady economic growth. That era is now changing. Trade fragmentation, rising geopolitical tensions, and supply chain reshoring are reshaping inflation dynamics, capital flows, and market leadership. In this new environment, the assumptions that supported passive investing are becoming less reliable. As correlations weaken and volatility increases, the ability to adapt becomes critical. In this piece, Stone Creek Advisors CIO and Co-Founder, Kasey Wopperer, examines how deglobalization is transforming the investment landscape and why active management may be essential for navigating the structural shifts ahead.

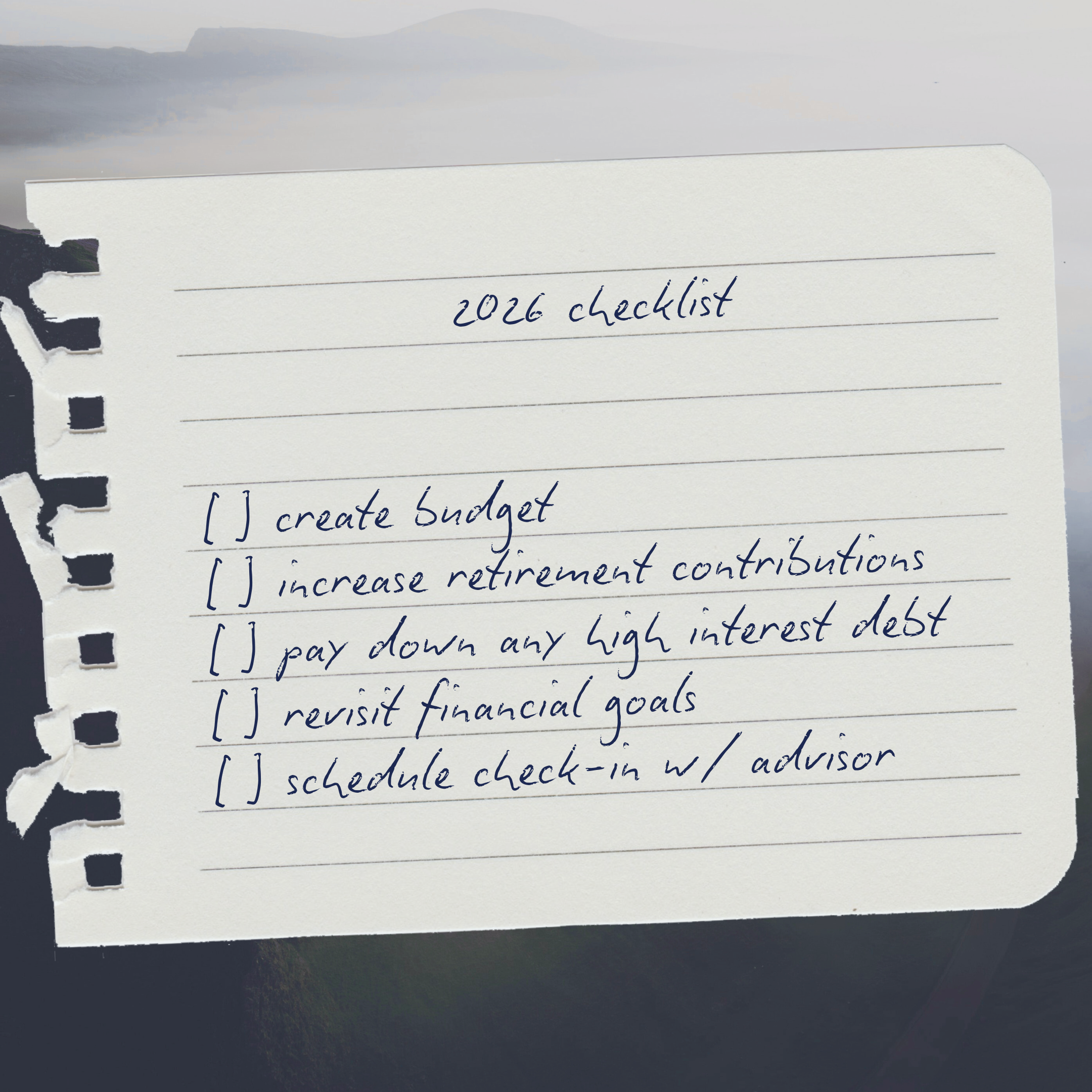

Essential Tips to Secure Your Financial Future in 2026

Start 2026 on the right financial footing with these 5 essential tips. From refreshing your budget and increasing retirement contributions to paying down high-interest debt and revisiting financial goals, this guide helps you take control of your money. Learn how proactive planning can secure your future and build lasting wealth.

2026 Retirement Contribution Limits: What You Need to Know

The IRS has increased 2026 retirement contribution limits, giving savers more opportunities to grow tax-advantaged assets. Learn what’s changed for 401(k), 403(b), and 457(b) plans, including higher employee deferral and catch-up limits, as well as updated IRA and Roth IRA contribution and income phase-out rules. This overview breaks down the key updates and what they mean for your retirement planning.