2026 Second Quarter CIO Letter: If Scarcity Ends

Written July 14, 2026

Kasey Wopperer, Co-Founder & CIO of Stone Creek Advisors

Key Takeaways:

The first half of 2026 has rewarded optimism. Earnings strengthened, AI investment continues to accelerate, and markets have recovered to new highs.

Momentum and leverage have reached historically elevated levels. Expectations leave less room for disappointment than they have in several years.

Today's market may be entering a new phase. For nearly twenty years investors benefited from shrinking public equity supply. That tailwind may now be reversing.

Future returns may depend less on multiple expansion and more on free cash flow generation, capital allocation, and returns on invested capital.

Technology revolutions create enormous wealth, but they have historically also attracted too much capital. AI may ultimately follow a similar path.

We remain constructive on long-term innovation while emphasizing diversification, valuation discipline, and businesses capable of generating durable free cash flow.

Today: Why Optimism Feels Justified

By almost any measure, the first half of 2026 has been encouraging. Corporate earnings have exceeded expectations, Artificial Intelligence (AI) remains one of the most exciting technological developments in decades, productivity has begun to improve, and despite geopolitical shocks, the U.S. economy continues to expand.

AI is becoming one of the largest investment cycles in history. Investors have rewarded companies they perceive to be on the right side of the transformation. Businesses in every industry are racing to understand how AI will reshape their operations.

Technological revolutions have repeatedly created enormous economic value. Railroads, electrification, personal computers, and the internet all reshaped the economy despite periods of excessive speculation.

The American economy has repeatedly demonstrated an extraordinary ability to reinvent itself during technological change. We believe this time will be no different. However, great innovations are not always great investments, especially if expectations are too optimistic.

The Power of Momentum

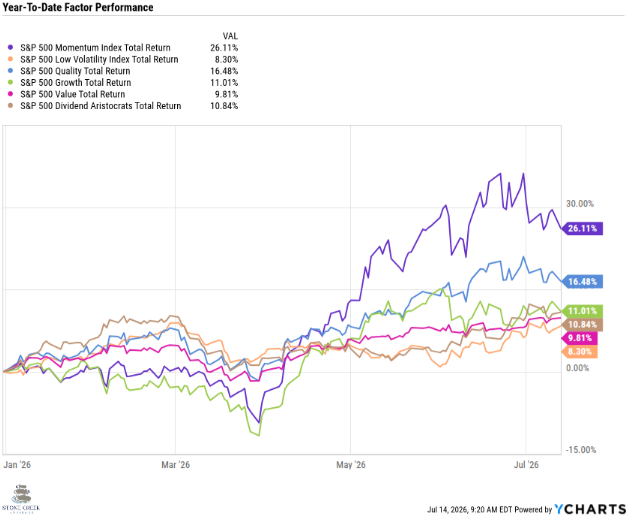

Following the Spring selloff, the S&P 500 rallied to new highs, fueled largely by AI enthusiasm. Momentum dominated as the S&P 500 Momentum Index returned 26% through July 13th. Leadership has shifted with the Magnificent Seven largely flat year-to-date, allowing the equal-weighted S&P 500 to outperform the traditional cap-weighted index. Value, small caps, and quality have also strengthened.

The picture is not as broad as headline performance suggests. This has been a shift from hyperscalers to AI spending beneficiaries. Anything not tied to AI has acted as an anti-AI trade, investing became a choice between AI and everything else. Breadth has remained narrow and rolling 65-day average correlations in the Russell 1000 fell to 0.2 on July 9th, one of the lowest readings in data back to the 1980’saccording to Jeffrey deGraaf, CEO of Renaissance Macro Research.[1]

Strong momentum usually reflects improving fundamentals and growing investor confidence. However, history suggests unusually strong momentum tends to mark an extreme which leads to muted forward returns. Very narrow participation tends to occur in environments where conviction is low, and the bull market may be fading. Forward returns tend to be negative following these periods. Neither tells us when sentiment will shift and these periods tend to persist longer than expected, but expectations have become increasingly difficult to exceed, leaving very little room for disappointment.

Margin debt has risen sharply since early 2024 and is on the brink of an extreme. Since 1997, when our “Margin Debt as a Percentage of Market Cap” indicator has entered the extreme signal, the median forward 12-month return has been -13.5%. Extreme readings rarely last because margin debt can be such a powerful negative force when volatility arrives. As markets decline, margin calls force additional selling, creating a feedback loop and accelerating losses. We are more concerned today because this is not just a U.S. issue and because some retail investors are using margin to buy leveraged ETFs, effectively layering leverage on top of leverage.

Momentum can be just as powerful on the way down as it is on the way up. Diversified portfolios often lag during periods of narrow leadership. The alternative, however, is accepting a level of concentrated risk that history has repeatedly shown can become very painful when leadership changes.

We are not investing to outperform over a few quarters. Successful long-term investing requires an understanding of what today's prices already assume about tomorrow. We believe the long-term outlook remains constructive, but think returns are unlikely to surpass the last three years.

The Hidden Tailwind: Scarcity

One of the quietest and least appreciated tailwinds to U.S. equities over the past two decades was the steady reduction in the number of businesses and shares available to own. Shrinking public markets, aggressive buybacks, and rising demand supported higher valuations, rewarded companies that consistently repurchased stock, and amplified returns.

Stock prices are driven by supply and demand. When demand grows faster than supply, prices tend to rise. When supply grows faster than demand, returns become harder to generate.

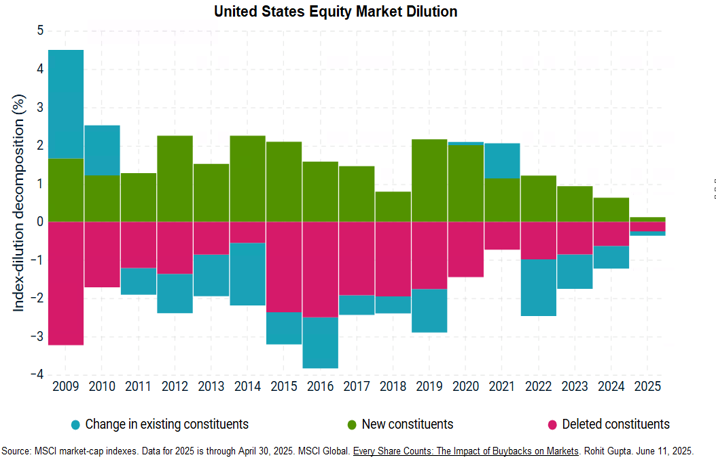

Going public used to be the natural destination for successful businesses. Public markets provided growth capital, liquidity for founders, and participation opportunities for investors. That changed drastically in the late 1990s. The number of publicly listed domestic companies in the U.S. peaked in 1996 at 8,090 before declining to 3,980 in 2025, according to the World Bank Group.[2]

Multiple forces drove this trend: the rise of private equity, the expansion of venture capital, increased regulatory burdens and costs associated with public listings, and mergers and acquisitions. Firms stayed private for longer, often reaching enormous scale before an IPO, and many never went public at all.

This resulted in a structural reduction in the supply of investable public equities while retirement contributions, passive investing, global capital flows, and quantitative easing directed increasing capital toward that shrinking pool. Few markets benefit more than one with rising demand and falling supply.

The decline in public companies was only part of the story. Over the same period, corporations repurchased trillions of dollars of their own stock. According to S&P Global, after 1997, share repurchases surpassed dividends as the primary method of returning capital to shareholders. By 2018, 53% of companies were repurchasing shares compared with just 28% in 1980, while the percentage paying dividends had fallen from 78% to 43%. [3]

At its simplest, buybacks reduce the number of shares outstanding, increasing each remaining shareholder's future earnings and free cash flow claim. Buybacks gained favor for numerous reasons: tax rates on capital gains versus dividends, SEC repurchase activity rule changes, ability to defer capital gains, management flexibility, sector composition, capital structure adjustments, takeover defense, stock option offset, and a signal of management confidence. Less supply competing for more demand.

The Next Chapter May Look Different

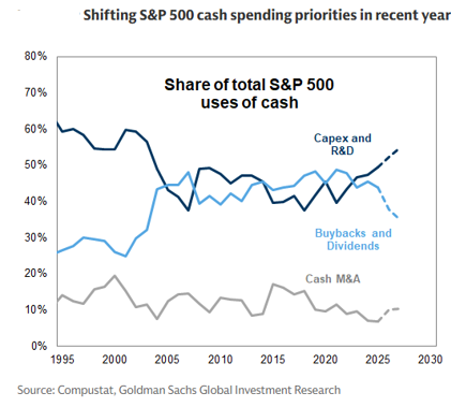

We don’t expect net public equity supply to expand overnight. Buybacks will likely remain healthy. But enough is changing to question whether the tailwind will remain. AI investment is extraordinarily capital intensive. Companies will fund investments with operating cash flow, while others issue debt or equity.

When businesses generate excess cash, management has three primary choices: reinvest in the business, return capital through dividends, or repurchase shares. Historically, distributing the cash to shareholders has been viewed as more shareholder friendly.

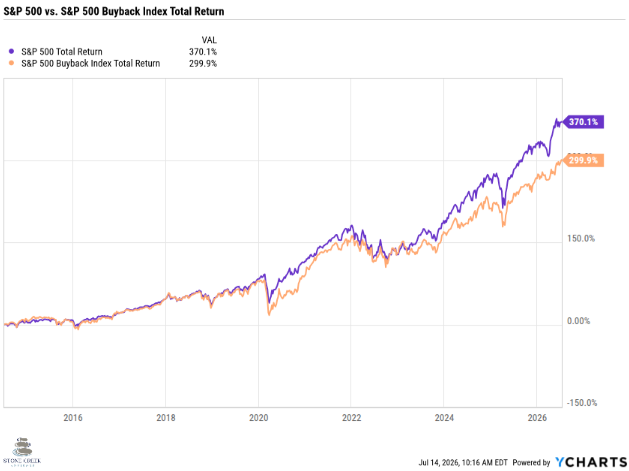

AI is changing how companies allocate capital and who is rewarded. Since late 2024, the Buyback Index has underperformed the S&P 500. Capital allocation follows incentives. If markets reward AI investment over shareholder yield, management teams are likely to direct cash toward growth. Hyperscalers reduced their buybacks by 64% in the first quarter.

The IPO pipeline is the healthiest it has been in years. SpaceX has already gone public, and companies such as OpenAI and Anthropic could follow. The potential pipeline (including SpaceX and SK Hynix that already occurred) could approach $4 trillion of market value, ~6% of today's U.S. equity market. [4]

IPO waves often appear during periods of strong investor confidence and have been viewed as a sign of optimism. Businesses prefer raising capital when markets are receptive. IPOs themselves are not negative, and many become exceptional long-term investments. However, they increase the supply of publicly traded securities competing for investor capital. Companies generally choose to sell stock when capital is abundant and valuations are attractive, not when markets are depressed. Major IPO waves have often coincided with periods of elevated investor enthusiasm and, at extremes, below-average subsequent market returns. The IPO itself is rarely the problem. Rather, additional supply absorbs capital that previously supported existing public companies.

Debt markets are changing as well. Debt financing has been imperative in the AI investment cycle. Goldman Sachs Research estimates over $600 billion in AI-related debt has been issued across the hyperscalers, their suppliers, and data center construction since 2024.[5] Hyperscaler net debt alone has increased from $69 billion at the beginning of 2025 to approximately $206 billion. [6]

For much of the last two decades, investors benefited from a shrinking supply of public equities supported by aggressive buybacks and limited new issuance. The next phase may look different, especially as the lockup periods following these IPOs expire. If AI drives higher capital spending (capex), more debt and equity issuance may follow, potentially expanding financial asset supply.

Future returns may depend less on multiple expansion and more on free cash flow generation, disciplined capital allocation, and the ability to earn attractive returns on invested capital.

Earnings Matter. Free Cash Flow Matters More.

One of the more encouraging developments over the past twelve months has been the S&P 500 return has been entirely earnings driven. For several quarters, we argued multiples had already expanded about as far as could reasonably be expected and any equity market strength from here needed to come from earnings catching up. To their credit, they have.

According to Goldman Sachs, first-quarter S&P 500 earnings grew 17% (excluding one-time items), and expectations for future growth remain high. Second quarter consensus calls for 22% year-over-year earnings growth, the strongest outlook entering an earnings season since 2021. Goldman Sachs estimates companies tied to AI will generate nearly 60% of overall S&P 500 earnings growth in Q2, with NVIDIA and Micron alone contributing over 40%.[7]

Strong earnings have justified the market's recent optimism, but not all earnings are equal. One of the more interesting developments this earnings season has been the growing contribution from non-operating gains. According to Baolian Wang, more than twelve cents of every dollar of S&P 500 earnings generated in Q1 came from the “Other Income and Expenses” lines of Alphabet, Amazon, and Nvidia’s Income Statements. Those gains increased reported earnings by roughly 12% and earnings growth by nearly 75%.[8]

Historically, this line item has been stable and designed for items outside a company’s main operations (interest earned on cash reserves, foreign exchange fluctuations, etc.). Much of this reflects unrealized gains on venture investments that accounting rules now require companies to recognize through their income statements as valuations increase. This includes markups on startups they invested in that raised new private funding rounds at higher valuations. These gains do not reflect improvements in underlying business operations and are NOT CASH management can use.

As Wang notes, approximately 60% of Alphabet's, 51% of Amazon's, and 27% of NVIDIA's reported net income came from non-operating, unrealized gains. Those gains may not recur if private market valuations stabilize or may even decline. Earnings are strong without them, but their quality is different than operating earnings.

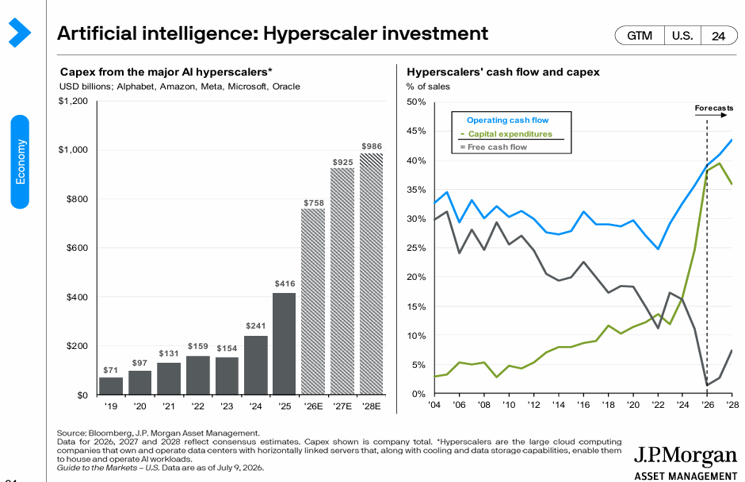

The AI buildout requires unprecedented investment in data centers, networking equipment, semiconductors, power infrastructure, and cooling systems. Expected capex among the largest hyperscalers exceeds previous technology investment cycles. J.P. Morgan estimates they could spend $758 billion on capex in 2026 and $925 billion in 2027, roughly 100% of their projected operating cash flow. [9]

During periods of extraordinary investment, free cash flow is in focus because it determines how much capital remains available for shareholders after funding future growth. Absent cash on the balance sheet, spending above free cash flow requires companies to issue shares or debt to pay for the costs, putting more equities and bonds into the market and increasing supply.

A company’s balance sheet could look relatively healthy, their earnings could look strong because of the way capex appears on the income statement, but their cash flow could be going to capital spending. Free cash flow is one of the best predictors of future returns and has always been our preferred factor.

The Tech sector has the biggest required capital investment, changing the way the sector has historically operated and the characteristics that commanded such high multiples. Over the past two decades, the sector has been defined by high margins, modest capital spending, limited leverage, abundant free cash flow, and large buybacks. Spending in hopes of future growth may create tremendous long-term value but requires cash today. As free cash flow becomes increasingly constrained, we question whether the same multiples will be attached to a sector that looks so different.

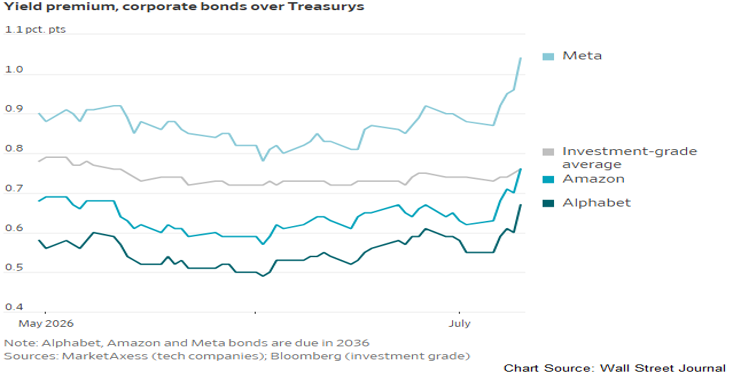

Investors are beginning to recognize that distinction. Scrutiny of free cash flow, capital spending, debt issuance, and returns on invested capital (ROIC) is increasing. Markets are no longer rewarding AI spending simply because it is large. They want evidence these investments will generate attractive returns. Over the past few weeks there has been $75 billion in bond issuance from AI-related companies and investors are showing a demand for a higher yield to absorb these bonds. [10]

If free cash flow becomes consumed by AI infrastructure, buyback activity may slow and debt issuance, IPO activity, and secondary offerings may increase. Scarcity ends.

This path is not set in stone. If investors, once again, place greater emphasis on free cash flow generation and capital discipline, hyperscalers may come under increasing pressure to moderate their capital spending. While such a shift would likely strengthen the financial position of the hyperscalers, it could create problems for many of today's AI infrastructure beneficiaries. Much of their premium valuation assumes current spending levels persist for years to come, meaning any slowdown in investment could have an outsized impact on revenue expectations and, ultimately, valuations.

Technology Revolutions Have Always Attracted Too Much Capital

Historically, investors preferred money in their pocket over a company reinvesting in growth because history shows companies tend to do irresponsible things with their money.

Paul Kedrosky recently made the observation that if today's AI buildout avoids a bubble, it would be the first major infrastructure investment cycle in roughly two centuries to do so. History follows a familiar pattern. Investors correctly identify a technology that changes the world but collectively overestimate how quickly it will be adopted, how much capacity is needed, and how profitable every participant will become. Each time, the technology changed the world and there were great investment opportunities, but investors often became so optimistic about the opportunity they collectively invested more money than economic returns could justify (an investment bubble).

· The canal boom of the 1830s dramatically lowered transportation costs and transformed commerce throughout the U.S.

· Railroads in both Britain and the U.S. permanently changed trade, industrialization, and the movement of goods and people.

· Electrification reshaped manufacturing and laid the foundation for the modern economy.

· The internet revolution fundamentally changed communication, commerce, and daily life.

Bubbles are not uncommon. They occur in industries and specific asset classes, but do not impact the entire global economy like massive infrastructure buildouts do. It is impossible to predict when a bubble will burst, and it is difficult to identify the bubble while you are in it. The immensity of spending is challenging to track as everyone is moving fast and at once to gain share, making it tough to know if the capacity being built has detached from economic rationale.

Given the immense amount of money chasing this opportunity, AI infrastructure spending deserves scrutiny. It is questionable if returns can match the scale of the investment. U.S. spending on data centers has heavily influenced GDP over the past 18 months and spending is increasingly being driven by lending. According to Grant’s Interest Rate Observer’s July 3rd note, “AI-related spending is projected to make up 2.1% of GDP this year, approximately the same as the railroads’ contribution between 1850 and 1859.”[11]

In each prior bubble, companies and investors correctly identified the future, but often overestimated how quickly that future would arrive and how profitable every participant would ultimately become. History suggests as breakthrough technologies mature competition increases, prices fall, and much of the economic value shifts away from the builders of the infrastructure and toward the businesses that successfully apply it.

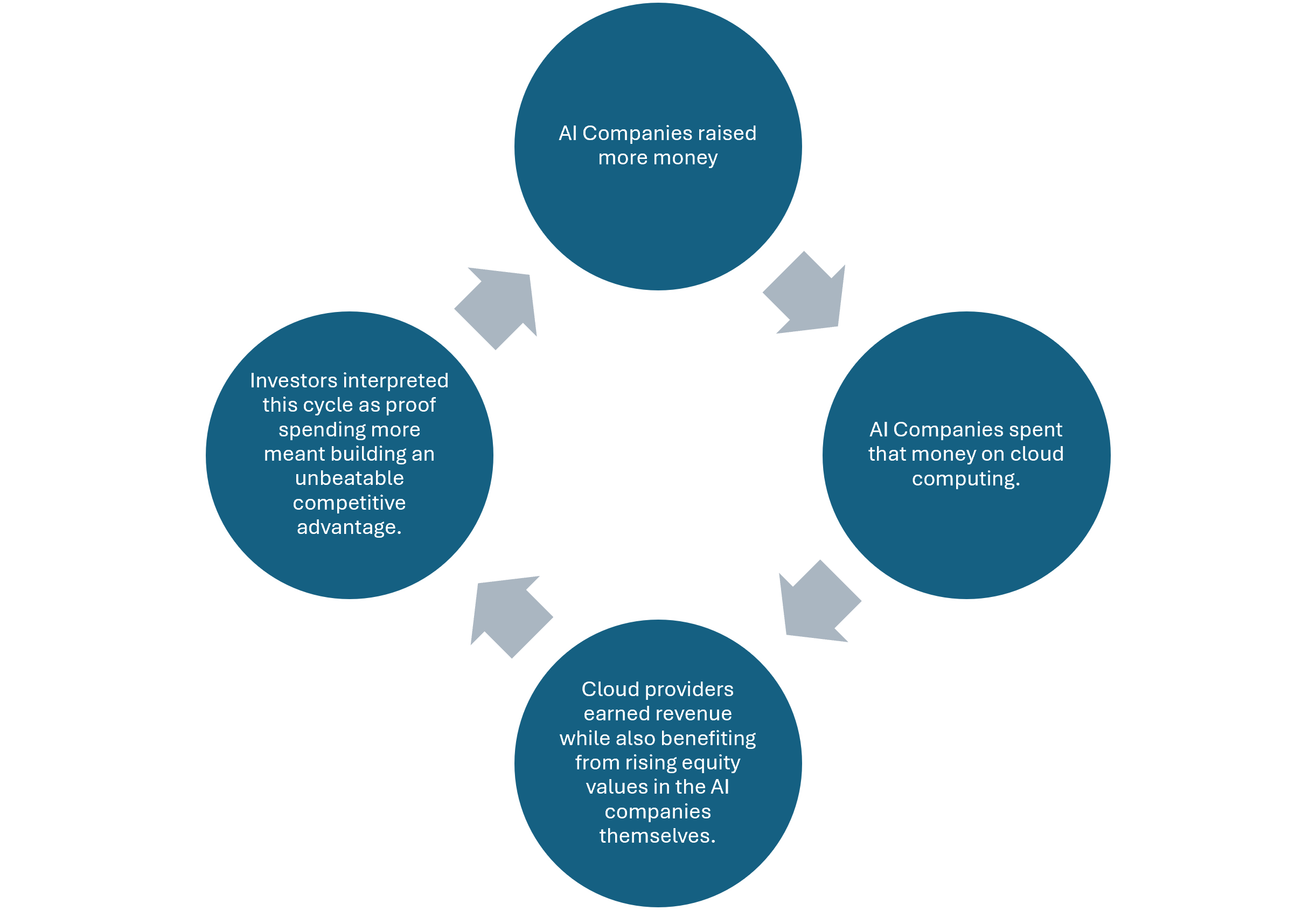

Phase One—The Builders: In the first phase of new technology, bigger is better. The first wave of AI rewarded companies that spent the most money building cutting-edge AI models that required billions of dollars of computing power, specialized chips, and massive data centers. Portions of the ecosystem are simultaneously acting as investor, customer, and supplier, making it difficult to distinguish between demand created by end users and demand created by the investment cycle itself. Circular financing is a unique aspect of today’s AI investment cycle that deserves attention.

Jared Grogan’s March 9th paper describes the process. Hyperscalers invest billions of dollars into foundation model developers whose developers spend the capital purchasing cloud computing from the same companies that invested in them, flowing back into hyperscalers’ revenue. That high-margin cloud revenue justifies higher valuations, encouraging another, higher valuation, funding round, leading to more infrastructure spending and another round of revenue.

“The hyperscalers earned returns on both sides of each transaction: equity appreciation in the foundation model company, and high-margin revenue on the infrastructure the company was required to purchase — revenue generated at the economics of scaled cloud, where each additional dollar of workload spend contributes disproportionately to operating income. High pre-training costs, far from being an unavoidable technical constraint, were the mechanism that made the structure work — creating the appearance of a capital-intensive moat that suppressed competition while justifying each successive valuation increase.”[12]

The hyperscalers are essentially setting the price for AI training models, knowing they are getting the cloud compute money. This may continue until we have another DeepSeek-like moment where the cost to train is much lower, resetting the high training costs.

Phase 2—Commoditization: In early 2025, China’s DeepSeek demonstrated an AI model could deliver similar performance for a fraction of the training costs. The market seems to have discounted this fear, but this may be an important turning point in the story. New AI models are approaching similar levels of performance while requiring drastically less computing power and significantly lower development costs.

Grant’s provides evidence that companies that have blown through their AI budgets are rationing AI use or moving to cheaper start-ups, many of them Chinese, as the performance gaps have narrowed. Both Anthropic and OpenAI are discussing major price cuts which means these monopoly-like prices being extrapolated into the future are unlikely to continue.[13] AI models start to become more commoditized, lowering differentiation for all players on anything but price.

The more efficient AI becomes the more computing costs could fall, the more competitors enter the market, the more prices could decline, and the more profit margins may compress. Historically, the technology succeeded, but the early infrastructure providers often didn’t. While OpenAI and Anthropic are talking about price cuts, we are still seeing major price increases for new computing power as data center capacity is still ramping up. According to the Wall Street Journal, Jensen Huang “recently estimated the cost of building a gigawatt of new computing power using his company’s architecture could soon reach $80 billion to $100 billion. Some operators have been forced to seek deeper-pocketed backers to fund their next phase of expansion, according to several people working on the deals.”[14]

During this phase technology becomes more efficient. During the dot-com era telecom companies spent a lot of money laying fiber-optic cable because they expected internet traffic to grow forever. It did, but technological advancements dramatically increased the amount of data each cable could carry resulting in a glut of fiber, collapsing prices. Many of the companies which financed the buildout went bankrupt.

The likelihood of overbuilding is high. A lot of AI may end up running on actual devices which may decrease demand for data centers leading to a glut in capacity that SO MUCH MONEY is being spent on.

Phase 3—The Users:Companies able to incorporate AI into their service offerings and business models to boost revenues should start to be rewarded. Software could be an example. The infrastructure itself could become commoditized, but the applications built on top of them can still be very valuable.

Phase 4—The Beneficiaries:In the final phase the true beneficiaries of AI are likely to prevail. Goldman Sachs estimates that widespread AI adoption would have a 1.5% annual impact on productivity growth in Developed Markets.[15] The long-term beneficiaries of AI are companies that will utilize the technologies to increase efficiencies within their organizations, especially as the costs of AI come down. The market is not yet rewarding beneficiaries of the technology for any future margin expansion. Just as inexpensive electricity created enormous opportunities for appliance manufacturers and industrial companies, inexpensive AI could create outsized value for businesses across industries.

Investments in all phases could prove exceptionally attractive over the long run, but valuations for the companies in the first two phases are exceptionally high. The near-term beneficiaries of AI are well understood, and the market has already reacted. However, the true long-term beneficiaries of AI have barely moved. While our portfolios have exposure to all phases, we have meaningful exposure to the last two phases, companies positioned to benefit from the transformation, but which is not yet reflected in prices.

The Bank for International Settlements (BIS) 2026 Annual Report highlights these historical parallels. Their work notes that transformational technologies frequently attract waves of investment that extend well beyond what near-term commercial demand can support.[16] There is, however, new pushback on these data centers which could alleviate the overbuilding potential. On July 14th, the Wall Street Journal reported that New York Governor Kathy Hochul is ready to sign an executive order that would ban construction of data centers of 50 megawatts or more in New York for a year while they create regulations, following other cities and counties who have issued temporary stops on construction.[17]

Much of today's spending may prove to be exactly what is required to build the infrastructure that supports the next generation of economic growth. But do current valuations already assume every dollar of capital being invested today will earn an attractive return?

Ushering In a New Era at the Fed

Kevin Warsh is the new Fed chair. He joined the Fed Board in 2006, becoming the youngest ever Governor appointed. As a voting FOMC member he participated in the major decisions of the 2008 Financial Crisis. During his time, he gained a reputation of being very hawkish. He resigned from the Board in 2011 over belief the Fed holds rates too low, expands its balance sheet too freely, and overreaches its mandate.

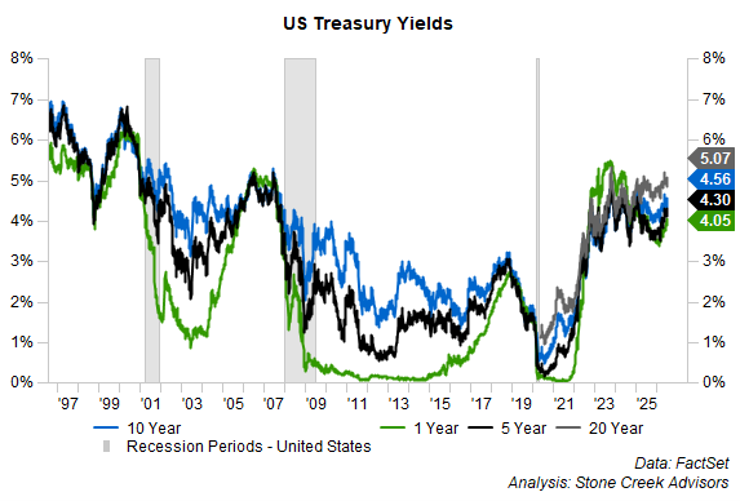

President Donald Trump seems to believe he would cut rates. However, with Chair Warsh inheriting the current economy and renewed inflation pressures, that seems increasingly unrealistic today. Internal dissents within the Fed are the highest since 1992. As of July 6th, only 23.2% of participants see rates unchanged through the December meeting, with 42.1% expecting one hike and the rest expecting more.

Independence is extremely important to maintain, and stability should be prioritized over political pressure. If independence is questioned long-term rates will likely move higher. Further inflation risks could also push yields higher. US Treasury yields matter, especially the ten-year, because borrowing costs globally are benchmarked off them.

Chair Warsh has consistently spoken about shrinking the balance sheet. Following through would effectively increase the amount of debt private investors must absorb. The amount of global government debt has been anything but scarce for a while now and a lot of debt needs to be rolled over this year. Removing the price insensitive buyer from the market would likely push yields higher.

Positioning for the Next Phase

Innovation will create tremendous opportunities. We continue to believe companies trading at valuations that provide reasonable long-term return potential and are generating healthy free cash flow and strong balance sheets, maintaining pricing power and durable competitive advantages, and investing thoughtfully in future growth will add value over the long-term.

We continue to find opportunities internationally, maintain some exposure to gold as a portfolio diversifier, favor shorter-duration fixed income given ongoing fiscal uncertainty, and selectively add to areas where market pessimism has created attractive valuations rather than chasing momentum.

AI will reshape the economy over the coming decade, but every AI-related investment will not generate attractive returns. History suggests technological revolutions often produce extraordinary winners alongside periods where investor expectations outpace economic reality. We are constructive on parts of the AI story but disciplined about what we pay.

Markets tend to extrapolate recent history. Most investors have spent their careers investing during a period characterized by declining interest rates, demographic dividends, falling corporate tax rates, globalization, a U.S. exceptionalism premium, abundant liquidity, aggressive corporate buybacks, and shrinking public equity supply. Collectively these tailwinds created an environment in which owning equities became easier.

As these tailwinds change, future returns may depend less on expanding valuation multiples and more on business fundamentals, free cash flow generation, and thoughtful capital allocation. The market may transition toward an environment where selectivity matters.

None of this is set in stone and our role has always been to adjust as the data adjusts. The picture may change and our portfolio will change with it. Our responsibility is to thoughtfully steward capital through changing market environments, participate in long-term wealth creation, and remain disciplined when expectations become disconnected from fundamentals.

As always, please reach out with any questions.

Kasey

Stone Creek Advisors is a DBA of OneSeven, an investment adviser in Ohio. OneSeven is registered with the Securities and Exchange Commission ("SEC"). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. OneSeven only transacts business in states in which it is properly registered or is excluded or exempted from registration. A copy of OneSeven's current written disclosure brochure filed with the SEC, which discusses OneSeven's business practices, services, and fees, is available through the SEC's website at: www.adviserinfo.sec.gov. All titles listed for Individuals associated with Stone Creek Advisors represent the individual's role with Stone Creek Advisors.

Please note, the information provided in this presentation is for informational purposes only and investors should determine for themselves whether a particular service or product is suitable for their investment needs. Please refer to the disclosure and offering documents for further information concerning specific products or services. Investments in securities entail risk and are not suitable for all investors. Past performance is not a guarantee of future returns. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

[1]Low Stock Correlation Signals Opportunity for Alpha | Jeffrey deGraaf, CMT, CFA posted on the topic | LinkedIn

[2]Listed domestic companies, total - United States | Data

[3] Examining Share Repurchases and the S&P Buyback Indices

Chart 2: Every Share Counts: The Impact of Buybacks on Markets | MSCI

[4] Why IPO mania could signal top of the market

[5] Tracking credit-funded AI datacenter buildsThe Credit Line. July 6, 2026.

[6]More AI capex at the expense of buybacks

[7] S&P 500 Q2 2026 earnings season preview US Weekly Kickstart. June, 26, 2026.

[8] https://baolianwang.substack.com/p/the-69-billion-mirage-how-an-accounting

[9] JP Morgan Guide To The Market. July 9, 2026. J.P. Morgan Asset Management

[10] https://www.wsj.com/finance/investing/the-quarter-trillion-dollar-onslaught-of-ai-bonds-is-testing-investors-limits-e4cd2bda?mod=Searchresults&pos=2&page=1

[11] Grant’s Interest Rate Observer. July 3, 2026. AI Outsmarts Itself.

[12] Grogan, Jared. (2026). The End of the Foundation Model Era: Open-Weight Models, Sovereign AI, and Inference as Infrastructure. 10.48550/arXiv.2604.06217. https://www.researchgate.net/publication/403641426_The_End_of_the_Foundation_Model_Era_Open-Weight_Models_Sovereign_AI_and_Inference_as_Infrastructure

[13] https://www.wsj.com/tech/ai/openai-considers-drastic-price-cuts-anticipating-war-for-users-with-anthropic-9b8c178e?mod=Searchresults&pos=1&page=1

[14] https://www.wsj.com/finance/investing/data-center-builders-are-racing-to-offload-stakes-worth-billions-1a7d92f8

[15] Goldman Sachs Asset Management. “Perspectives on Artificial Intelligence”. Market Strategy. Strategic Advisory Solutions. 2026.

[16] BIS 2026 Annual Report. Annual Economic Report 2026

[17] https://www.wsj.com/us-news/new-york-set-to-temporarily-ban-large-new-data-centers-3755924c?mod=WTRN_pos1